|

Release Date: January 25, 2021 |

|||

CALFRESH

63-502 - Income Definition, Exclusions and Deductions

( ) To release a new policy

( ) To release a new form

( ) To convert existing policy to new writing style only – No concept changes

( X ) Revision of existing policy and/or form(s).

What changed?

This release provides revisions to the allowable Excess Medical Expense deductions, clarification on the verification requirements, and results for mid-period changes. Additionally, this release provides guidance on how to treat one-time-only medical expenses or expenses that are billed less than monthly. This release also provides a revision to the Standard Deduction for Federal Fiscal Year 2019-2020.

This release will further discuss the following in detail:

· Income

· Income for Excluded Household (HH) Members

· Income and Expenses for Non-HH Members

Note: Unearned and Self-Employment income will be discussed in a separate document. Changes are shown highlighted in grey throughout the document.

Income is defined as all money received, regardless of the source. CalFresh policy further categorizes the income received under different types and treats each type differently. Furthermore, each income type has different sub-categories that are also treated and counted differently when determining CalFresh eligibility. Certain types of income are excluded from being counted as income. Excluded incomes are types of income that are not counted as gross income before applying the ‘gross income test’ and prior to computing the ‘net income test.’ CalFresh policy allows for specific types of deductions, such as medical or dependent care expenses. These deductions are used in determining eligibility for the CalFresh Program.

N/A

|

Term |

Description |

|

Earned Income |

Earned income is that which is received in exchange for compensation for work performed.

Types of Earned Income:

· All wages, commissions, salaries, and tips of an employee; · Self-employment income; · Income derived from rental property only when a member of the HH is actively engaged in the management of the property at least an average of 20 hours per week (if this requirement is not met, then the rental income is to be considered unearned); · Income received from In-Home Supportive Services (IHSS) regardless if the recipient of care is in the home or not; · Income received from childcare providers; · College work-study income that is not funded by State/ · Training allowances from vocational and rehabilitation programs recognized by federal, State, or local governments, if they are not a reimbursement; · Any portion of striker’s benefits which are received as compensation for picketing; · All AmeriCorps payments are considered earned income although some types might be exempt (please see the section under AmeriCorps Payments for a more detailed description); · Vacation Pay; and · Census Worker income. Please note that earned income from temporary Census employment is excluded. This policy applies from August 1, 2020, through September 30, 2020. If the earned income is related to the 2020 United States (U.S.) Decennial Census Operation, it must be excluded regardless of when the temporary Census Bureau employee was hired. All 2020 U.S. Decennial Census-related positions are considered temporary due to the time-limited nature of the work. |

|

Income Exclusions |

Income excluded from the computation when determining CalFresh eligibility and benefit amount. Income exclusions are not counted when determining net income eligibility and benefit level. |

|

Income Deductions |

Income deductions are those amounts that can be subtracted from the gross countable income when determining net income eligibility and benefit level. |

|

Information on the application, Semi-Annual Report (SAR) 7, or recertification (RC) that is inconsistent with the statements made by the applicant, adult HH member, or Authorized Representative. To be considered questionable, information reported must be inconsistent with the statements made by the HH or inconsistent with other information received by the Eligibility Worker (EW), per MPP Section 63-300.5(g). |

|

|

Collateral Contact |

A collateral contact is an oral confirmation of the HH’s situation/statement by a person outside of the HH. |

CalFresh HHs must meet income limits set by the United States Department of Agriculture-Food Nutrition Service (USDA-FNS) for their HH size and other policy requirements to receive CalFresh benefits.

A standard income disregard of 20% is applied to countable gross earned income. The 20% income disregard is not applied to the income that was not reported by the HH and was later discovered through different reviews.

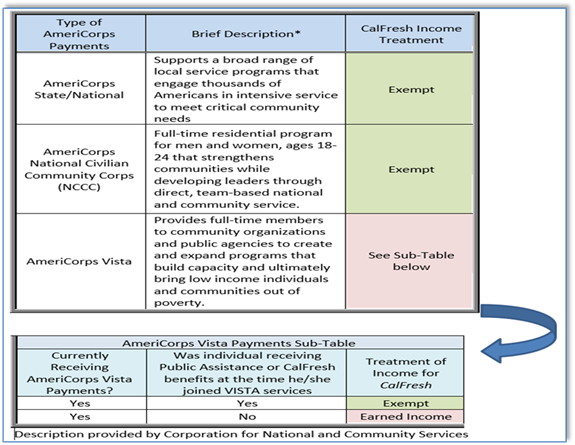

In 1994, Congress created the National Service Trust Act and transferred the Volunteers in Service to America (VISTA) Program to the Corporation for National and Community Service. Three programs were created:

· AmeriCorps State/National Program;

· AmeriCorps National Civilian Community Corps; and

· AmeriCorps VISTA (formerly known as VISTA).

The table below provides instructions on how to treat income from all three

AmeriCorps Programs:

INCOME EXCLUSIONS

Income exclusions must be disregarded when determining both CalFresh eligibility and benefit amount. As exclusions, these types of income are deducted from the gross income, before applying the ‘gross income test’ and prior to computing the ‘net income test.’ Income exclusions are calculated monthly and are; therefore, not factored. The following is a list of excluded income for the CalFresh Program:

|

Type of Excluded Income |

Description |

|

Allowances paid under Public Law 104-204 to children of Vietnam Veterans with specific conditions |

Allowances paid to children of Vietnam Veterans who are born with spina bifida. |

|

AmeriCorps State/ National, or AmeriCorps National Civilian Community Corps |

Payments from the AmeriCorps umbrella programs, including the National Civilian Community Corps. |

|

California Victims of Crime |

Payments received under California Victims of Crimes Program. |

|

Cash Donations |

Cash donations received from one or more private, non-profit, charitable organizations of not more than $300 in a calendar quarter (i.e., January – March, April – June, July – September, or October – December).

Note: Donations in excess of $300 in a calendar quarter is considered unearned income. |

|

Cash for Specific Purposes or Contributions from Persons or Organizations |

Payments specifically provided for identified expenses, other than normal living expenses, and used for the purpose intended. |

|

Census Income |

The Census Bureau employs for various positions including census takers, recruitment assistants, office staff, and supervisory staff. Only earned income received directly from the Census Bureau for temporary employment related to the 2020 U.S. Decennial Census must be excluded when determining CalFresh eligibility and benefits. |

|

Combat Zone Military Pay |

Additional income received by a member of the U.S. Armed Forces who has been deployed to a designated combat zone if the additional pay is the result of deployment to or while serving in a combat zone. |

|

Department of Rehabilitation Training Allowances |

Allowance for training expenses paid to recipients participating in Department of Rehabilitation training programs. |

|

Disaster Relief Employment Income during a nationally declared disaster |

This is income received from employment for a nationally declared disaster under a National Emergency Grant. |

|

Educational Assistance |

When not otherwise excluded by federal statute, to the extent that this is earmarked by the lender, used for, or intended to be used for, allowable educational expenses at qualifying institutions. The education assistance may be in the form of loans on which payments is deferred, grants, scholarships, fellowships, and veteran’s educational benefits. |

|

Earned Income of a child |

Earned income from children who are members of the CalFresh HH, in elementary or secondary school at least half-time and have not attained their 19th birthday. The exclusion continues to apply during temporary interruptions in school attendance due to semester or vacation breaks, provided the child’s enrollment will resume following the break. Individuals are considered children for purposes of this provision if they are under the parental control of another HH member. Determination of parental control is assumed when a child is residing with their natural, adoptive or stepparents. The following note applies when a child under 18 is residing with an adult other than their parent and parental control is in question.

Note: A minor child is not considered under parental control of an individual with whom he/she resides if:

a) The minor has entered a valid marriage; b) Is on active duty in any branch of the U.S. Armed Forces; or c) Has been emancipated by court order.

If none of the above applies, then eligibility staff must consider the following on a case in which parental control is being evaluated:

a) The degree to which the minor child is economically self-supporting and managing his/her own affairs; b) The proximity of the minor to the age of 18; and c) Whether the minor is absent from the adult for significant periods of time and comes and goes without the adult’s approval. |

|

Foster Care Payments |

Those foster care payments received by HHs with foster care boarders who are not part of the CalFresh HH. |

|

Independent Living Program (ILP) |

Income and incentive payments earned by a child 16-years of age and older who is participating in the ILP when income is received as part of the ILP written Transitional Independent Living plan. |

|

In-Kind Benefits |

Any gain or benefit which is not in the form of money payable directly to the HH, including non-monetary benefits, such as, but not limited to meals, clothing, housing, or produce from a garden. |

|

Legally Obligated Child Support (paid out) |

Legally obligated child support payments to a non-HH member are treated as income exclusion rather than an income deduction, for the individual making the payment. Child support payments made to a third-party (e.g., landlord or utility company), or made to obtain health insurance for a child on behalf of the non-HH member in accordance with the support order must also be excluded.

Note: Alimony or Spousal Support is not an excluded income. |

|

Loans |

All loans, including loans from private individuals and commercial institutions. When verifying whether income is exempt as loan, a legally binding agreement is not required. A simple statement signed by both parties which indicates that the payment is a loan and must be repaid shall be sufficient verification. However, if the HH receives payments on a recurrent or regular basis from the same source, but claims the payments are loans, the Department may also require that the provider of the loan sign an affidavit which states that repayments are being made or that payments will be made in accordance with an established repayment schedule.

Note: Educational loans on which repayment is deferred are not excluded income. |

|

Monies received and used for the care of a third-party beneficiary |

This applies when the beneficiary is not a HH member. If the intended beneficiaries of a single payment are both HH and non HH members, any identifiable portion of the payment intended and used for the care and maintenance of non HH members must be excluded. If the non HH member’s portion cannot be readily identified, the payment must be evenly prorated among the intended beneficiaries and the exclusion applied to non HH member’s pro rata share or the amount used for the non HH member’s care and maintenance, whichever is less. |

|

Non-Recurring Lump Sum Payments |

Lump-sum payments, such as income tax refunds, rebates, or credits, retroactive lump sum Social Security Administration benefits, railroad retirement benefits or retroactive payments from the approval of public assistance benefits. |

|

Reimbursements |

Reimbursements for past or future expense when they do not exceed actual expenses, and do not represent a gain or benefit to the HH. To be excluded, reimbursements must be provided specifically for an identified expense, other than normal living expenses, and used for that purpose. When reimbursement, including a flat allowance, covers multiple expenses, each expense does not have to be separately identified if none of the reimbursement covers normal living expenses. The amount by which a reimbursement exceeds the actual incurred expense must be counted as income. |

|

Relocation Assistance |

A relocation assistance benefit paid by a public agency to a HH that has been relocated because of development, urban renewal, freeway construction or any other public development involving demolition or condemnation of existing housing. |

|

Scholarship Awarded to a Dependent Child |

Any award or scholarship provided to, or on behalf of a dependent child based on the child's academic or extracurricular activity. |

|

Vendor Payments |

Income not legally obligated to be paid to the HH but which is paid to a third-party. If there is legal obligation for this payment, then the income will be considered unearned income. Deferred educational loans, grants, scholarships, fellowships, veteran’s educational benefits, and the like, are legally obligated to the HH and therefore are not vendor payments. An employer paying rent directly to the landlord is considered a vendor payment and should not be counted as income or a deduction. |

|

Work Study |

Income from State or federally financed college work study for the current school term. Work study income is paid monthly based on the hours the student works, and it is paid separately from loans and grants.

Note: Payments or reimbursements received from a college Work Study Program that are completely or partially funded by Title IV of the Higher Education Act are exempt. |

|

RESOURCES AND/OR INCOME EXCLUDED BY OTHER FEDERAL LAW |

|

|

Federal program benefits |

Such as the School Lunch Program, School Breakfast Program, etc. |

|

Reimbursements from the Uniform Relocation Assistance and Real Property Acquisition Policy Act of 1970 (Public Law [P.L.] 91-646, Sec. 216) |

This is income that was received as compensation and assistance for those individuals whose property was compulsorily acquired for public use under “eminent domain” law. |

|

Earned Income Tax Credits (EITC) |

EITC received before January 1, 1980, because of P.L. 95-600, the Revenue Act of 1978. |

|

Income from programs under the Workforce Innovation and Opportunity Act (WIOA) |

Allowances, earnings and payments to individuals in programs specified under the WIOA are to be excluded, except the earnings of individuals participating in on-the-job training programs. |

|

Payments or allowances made under any federal laws, except benefits under a State program funded under Part A of the Title IV of the Social Security Act, for energy assistance, such as the Low-Income Home Energy Assistance (LIHEAA), or from Housing and Urban Development or the Farmers Home Administration programs |

One-time assistance payments or allowances under federal or State laws for weatherization or emergency repair or replacement of heating or cooling devices are excluded. |

|

Financial Educational Assistance |

Financial educational assistance provided under any of the following:

a) A program funded in whole or in part under Title IV of the Higher Education Act; b) Bureau of Indian Affairs Student Assistance Programs; Title XIII, Indian Higher Education Programs, Tribal Development Student Assistance Revolving Loan Program; or c) Some Carl D. Perkins Vocational and Applied Technology Education Act. |

|

Payments received as a restitution pursuant to the Civil Liberties Act of 1978 |

Payments received by U.S. Citizens of Japanese ancestry and permanent resident Japanese immigrants who were interned during World War II or their survivors, and payments received by Aleut residents of the Pribilof Islands and the Aleutian Islands west of Unimak Island pursuant to Aleutian and Pribilof Islands Restitution Act, for injustices suffered while under U.S. control during World War II. |

|

Payments received from the Agent Orange Settlement Fund |

Payments received from any other fund established to settle liability claims by veterans or survivors of deceased veterans concerning Agent Orange under the Agent Orange Compensation Act of 1989. |

|

EITC payments received by any HH members as an advance payment or in the form of a lump sum |

These payments must be excluded for 12 months, provided the HH was participating in the CalFresh Program at the time of the receipt of the EITC payment. |

|

Federal major disaster and emergency assistance provided under the Disaster Relief Act of 1974, and comparable disaster assistance provided by States, and local governments |

These are payments received by individuals and or families from different organizations because of a major disaster. |

|

Payments received from the Radiation Exposure Compensation Trust Fund |

These are payments received by individuals for certain diseases attributed to radiation exposure pursuant to the Radiation Exposure Compensation Act of 1990. |

|

Veteran's Benefits Improvement and Health-Care Authorization Act of 1986 |

Any amount by which the basic pay of an individual is reduced under the Veteran's Benefits Improvement and Health-Care Authorization Act of 1986. |

|

Payments under Title I of the Domestic Volunteer Services Act |

These payments include but are not limited to VISTA, University Year of Action and Urban Crime Prevention Program to volunteers who were receiving CalFresh or public assistance at the time they joined the Title I Program, must be excluded as income only. In addition, those individuals who were receiving an income exclusion of VISTA or other Title I subsistence allowance at the time of conversion to the Food Stamp Act of 1977, must continue to receive the income exclusion for VISTA for the length of their volunteer contract in effect at the time of conversion. Temporary interruptions in the CalFresh Program participation shall not affect the exclusion once eligibility has been determined. |

|

Payment to volunteers under Title II of the Domestic Volunteer Services Act |

These payments include but are not limited to the Retired Senior Volunteer Program, Foster Grandparents Program, and Senior Companion Program and must be excluded as income only. |

|

Payments provided by the Senior Community Service Employment Program (SCSEP) under Title V of the Older Americans Act |

Fund received by individuals age 55 and over provided by the SCSEP under Title V of the Older Americans Act, must be excluded as income. |

|

Payments made under the following programs must be excluded as income |

The value of any childcare provided or arranged for, or childcare under the following programs:

· Title IV-A of the Social Security Act, including transitional childcare; · The At-Risk Block Grant; and · The Child Care and Development Block Grant. |

|

Allowances, earnings, and payments made under Title I of the National and Community Service Act (NCSA) of 1990, must be excluded |

The NCSA includes programs under the Serve America, American Conservation and Youth Corps, and National and Community Services subtitles. |

|

Payments made to individuals because they have been determined to be victims of Nazi persecution |

Payments based solely on being victims of Nazi persecution are excluded. |

Legally Obligated Child Support Payments

CalFresh HHs can claim a child support expense if the child support payment is made to non-HH member(s) and is not voluntary.

Legally obligated (court-ordered) child support is treated as an income exclusion, rather than a deduction. When this option is utilized, the 20% earned income deduction will be applied prior to the child support exclusion. Documentary evidence must be used as the primary source of verification.

The amount for the most commonly used deductions frequently changes due to increases or decreases in the Cost-Of-Living-Adjustment (COLA). These changes are implemented and released by the USDA-FNS and take effect every year on October first. The California Department of Social Services (CDSS) releases annually its list with the maximum allowable deductions. CalFresh policy also allows for other, more specific types of deductions such as medical or dependent care expenses. Allowable deductions are factored (unlike income exclusions). In other words, the frequency in which the HH pays a deduction is the frequency used in determining eligibility to CalFresh (i.e., If a HH reports a weekly dependent care expense, then we will use the weekly frequency when determining eligibility).

Allowable deductions are:

Homeless Standard Shelter Allowance

Excess Medical Expenses Deduction

Shared Living Expense Deduction/Treatments of Expenses Shared with Others

The standard deduction is allowed for each HH per month in an amount that is established under the yearly COLA released by the USDA-FNS. For more information on yearly COLA, refer to 63-504.39 CalFresh COLA.

Excess Shelter Deduction

This is a monthly deduction in excess of 50% of the HHs income after all other applicable deductions have been allowed. The excess shelter deduction must not exceed the current maximum, unless the HH contains a member who is elderly or disabled. CalFresh policy defines shelter costs as the continuing costs for the shelter occupied by the CalFresh HH such as:

· Rent;

· Mortgage or other continuing costs leading to ownership of the shelter, such as loan repayments for the purchase of a mobile home, including interests on such payments;

· Property taxes, State and local assessments, and insurance on the structure itself, but not separate costs for insuring furniture or personal belongings;

· The cost of heating and cooking fuel, cooling and electricity, water, sewerage, garbage and trash collection fees, the basic service and rental fee for one telephone, including tax on the basic fee, and fees charged by the utility provider for initial installation and utility. One-time deposits must not be included as shelter costs;

· Shelter costs for the home if temporarily not occupied by the HH because of employment or training away from home, illness, or abandonment caused by a natural disaster or casualty loss. This is allowed only if the HH intends to return to the home, and the home is not being leased or rented during the absence of the HH;

· Costs for the repair of the home which was substantially damaged or destroyed due to a natural disaster such as fire or flood. Shelter costs must not include costs for repair of the home that have been or will be reimbursed by private or public relief agencies, insurance companies, or from any other source;

· Home Association Fees (HOAs), parking space fees for mobile homes; or

· Any portion of the allowable shelter expense paid by a non-HH member is not counted for the CalFresh HH.

To be eligible to obtain the Excess Shelter Deduction, the HH must only indicate that they incur shelter expenses, type of expense, and the amount on the CalFresh application, recertification, or SAR 7 report.

Homeless Standard Shelter Allowance (HSSA)

This deduction is available to homeless HHs that are not receiving free shelter. Homeless HHs which incur, or reasonably expect to incur, shelter costs during a month, are eligible to the HSSA deduction without providing verification of the shelter costs. Higher shelter costs may be used if verification is provided. Homeless HHs which do not incur shelter costs during the month are not eligible for HSSA deduction.

Standard Utility Allowance (SUA)

HHs that incur heating or cooling costs separate and apart from their rent or mortgage payments are entitled to the SUA. The SUA is also to be given to HHs receiving energy assistance payments made under the LIHEAA of 1981. HHs receiving energy assistance under a different program may be eligible for SUA only if they continue to incur

out-of-pocket heating or cooling expenses in addition to the energy assistance.

The SUA is not to be pro-rated

If a CalFresh HH’s utility expenses exceed the SUA, the actual utility expense cannot be allowed when determining the CalFresh benefit allotment.

Note: HHs who are using the HSSA are not entitled to the SUA, because a utility component is already included in the homeless shelter deduction.

Limited Utility Allowance (LUA)

This allowance is given to HHs that do not incur heating or cooling costs but pay at least two other separate types of utilities. Allowable utilities include telephone, water, sewerage, and garbage or trash collection. The LUA must not be pro-rated when the CalFresh HH lives with an excluded/ineligible HH member(s), or when the HH shares utilities included in the LUA with another HH.

Telephone Utility Allowance (TUA)

This allowance is given to HHs that are not eligible for either SUA or LUA but incur a telephone cost only. This will be used only in instances where the HH has a house telephone, or in its absence, an equivalent form of communication, such as a cellular phone. The TUA must not be prorated when the CalFresh HH lives with an excluded/ineligible HH member(s) or when the HH shares the phone expense with another HH.

This is 20% of the HHs gross earned income. Earnings that are already excluded are not to be included in the gross earned income for purposes of computing the earned income deduction. This deduction is not credited in instances in which the county discovers that a HH failed to report its earned income.

The dependent care deduction is the actual cost for the care of a child under age 18 or an incapacitated person of any age in need of care.

Note: For this provision only, incapacitation refers to any permanent or temporary condition that prevents an individual from participating fully in normal activities including, but not limited to, work or school without supervision and that requires the care of another person to ensure the health and safety of the individual, or a condition that makes a lack of supervision risky to the health and safety of that individual.

There is no cap on the deduction for dependent care expenses. Dependent care expense is only allowed if the service is provided by someone outside the CalFresh HH and the HH makes an out-of-pocket payment for the service. This expense must not include any amount that is covered by a subsidy.

The deduction must be allowed only in the month the expense is billed or otherwise becomes due, regardless of when the HH intends to pay the expense. The dependent care cost will be allowed as a deduction when it is necessary for the HH to do any of the following:

· Accept or continue employment;

· Comply with CalFresh Employment Training (CFET) Program requirements or an equivalent effort to seek employment by those not subject to CFET;

· To actively seek employment; or

· Attend training or pursue education which is preparatory to employment.

The costs of care provided by a relative may be claimed as deduction so long as the relative providing the care is not part of the same CalFresh HH as the child or incapacitated adult receiving the care. The dependent care deduction cannot be allowed if another CalFresh HH member or excluded HH member provides the care.

The dependent care deduction may be anticipated:

· Based on the most recent month’s out-of-pocket expense, unless the HH is reasonably certain a change will occur.

Allowable Dependent Care costs

The following is a list of allowable dependent care costs:

· The costs of care given by an individual outside of the CalFresh HH, provider, or care facility;

· Transportation costs to and from the care facility; and

· Activity, such as looking for a job or other fees associated with the care provided to the dependent.

The Internal Revenue Services (IRS) standard mileage rate must be used to determine transportation expenses. This is calculated by multiplying the number of round-trip miles by the federal mileage reimbursement rate (current reimbursement rates can be found at www.irs.gov).

Excess Medical Expenses Deduction

The excess medical expense is the portion of medical expense in excess of $35 per HH, per month (excluding special diets) incurred by any HH member who is 60 years of age or older or disabled (as defined in MPP Section 63-102[e]). Spouses or other persons receiving benefits as a dependent of the disability recipient are not eligible to receive this deduction.

Effective October 1, 2017, HHs that contain at least one elderly or disabled member with verified medical expenses between $35.01and $155 will be granted a Standard Medical Deduction (SMD) of $120. HHs with medical expenses above $155 per month may verify and claim the actual expenses.

HHs entitled to Expedited Service are allowed a medical expenses deduction if they list medical expense amounts even if verification of those expenses is postponed. The verification must be provided prior to the second month’s issuance, or prior to the third month of participation when the HH applied after the 15th of the month.

|

Verified Medical Expenses |

Eligibility |

|

Under or equal to $35.00 a month |

Not eligible for medical deduction |

|

$35.01 to $155 a month |

Eligible for the SMD ($120) |

|

$155.01 a month and over |

Eligible to deduct actual expenses minus $35.00 |

SMD Verification Requirements

· SMD is a monthly deduction. Only verified recurring medical expenses or

one-time expenses (that can be averaged over 12 months) totaling $35.01 or more qualify for the SMD.

· When initially claimed, HHs must verify that they incur more than $35.01 a month in allowable expenses. Failure to verify medical expenses is not a basis for denying or discontinuing a CalFresh application or case.

· Fluctuating medical expenses may be allowed as deductions if regularly recurring, reasonably anticipated, and verified. HHs may elect to have fluctuating expenses averaged or have them deducted in the months that are billed or otherwise become due. If a recurring payment does not fluctuate, it would not be averaged.

· HHs may elect to have expenses that are billed less often than monthly averaged forward over the interval between scheduled billings. If a bill is averaged over the interval between billings, the expense can be allowed even if the bill was not received in the certification period. If there is no regularly scheduled billing interval, the expense may be averaged forward over the period the expense is intended to cover.

· HHs may also elect to have one-time only expenses averaged forward over the entire certification period in which they are billed. HHs reporting one-time only medical expenses during the certification period may elect to have a one-time deduction or to have the expense averaged out over the remainder of the certification period. Averaging begins the month the reported change becomes effective. When a HH elects to average a one-time medical expense, the HH medical expense is averaged over the remaining months of the certification period, and $35 is deducted from the average each month.

· In the case of a HH certified for 24 months that reports a one-time medical expense incurred during the first 12 months of the certification period, eligibility staff must give the HH the option of deducting the expense for one month, averaging the expense over the remainder of the first 12 months of the certification period, or averaging the expense over the remaining months in the certification period. One-time expenses after the 12th month of the certification period will be deducted in one month or averaged over the remaining months in the certification period, at the HH’s option.

· Medical expenses carried forward from past billing periods are not deductible, even if they are included with the most recent billing and actually paid by the HH.

Mid-Period Changes

· If a HH voluntarily reports and verifies an increase in medical expenses

mid-period, the new deduction amount must be determined for remaining months in the certification period.

o HHs may voluntarily report and verify medical expenses mid-period between $35.01 and $155, which would make them eligible for the SMD; or

o HHs may voluntarily report and verify medical expenses mid-period in excess of $155, which would make them eligible for the actual deduction, minus $35.00.

· If the voluntary report results in increased benefits, a supplement will not be issued for the month in which the increased expense was reported. Once verification has been submitted, benefits will be increased for the remaining months in the certification period.

Allowable Medical Expenses

The table below provides a list of the allowable medical expenses:

|

Allowable Medical Expenses |

|

Medical and dental care including psychotherapy and rehabilitation services provided by a licensed practitioner or other qualified health professional authorized by State law. |

|

Hospitalization or outpatient treatment, nursing care, and nursing home care, including payments by the HH for an individual who was a HH member immediately prior to entering a hospital or nursing home, provided by a facility authorized under law. |

|

Prescription drugs when prescribed by a licensed practitioner authorized under state law and other over-the-counter medication (including insulin) when prescribed by a licensed practitioner or other qualified health professional. In addition, costs of medical supplies, sick-room equipment (including rental) or other prescribed equipment are deductible. |

|

Health and hospitalization insurance policy premiums. |

|

Medicare premiums related to coverage under Title XVIII of the Social Security Act; any share of cost or spend down expenses for medical costs incurred by Medi-Cal recipients. |

|

Costs of securing and maintaining any animal specially trained to serve the needs of elderly or disabled program participants are allowable medical expenses. Examples of such animals include seeing guide dogs, hearing guide dogs, and housekeeper monkeys. Food and veterinarian bills associated with the service animal are also allowable costs. An animal must be specially trained to assist the CalFresh recipient in order for its associated maintenance costs (such as veterinary bills, food, and other expenses) to be allowable deductions. While specific types of training, credentials, or certifications are not required, if the animal has not been specially trained to assist the individual with the medical issue for which the animal is prescribed, it is not a service animal and its expenses are not deductible. A pet or a companion animal that a client already owns does not automatically become a service animal if the client is later prescribed a service animal. |

|

Eyeglasses or contact lenses (and lenses solution) prescribed by a physician skilled in eye disease or by an optometrist, dentures, hearing aids, and prosthetics (including assistive devices). |

|

Actual costs of public or private car transportation and lodging to obtain medical treatment or services, including to health care appointments and pharmacies, fitting for dentures, hearing aids, or glasses, and trips to the dentist. When a costlier means of transportation, such as a taxi or private auto is the only means available or has been determined by the county to have been reasonable and necessary given the individual's medical circumstances, the actual costs of such transportation must be allowed. There is no requirement that medical travel trips be within the county of residence. HHs must verify expenses if they claim the out-of-pocket, non-reimbursed cost for medical travel if elderly and /or disabled members by third parties such as public transportation, taxis, or ridesharing companies such as Uber or Lyft. |

|

Maintaining an attendant, homemaker home health aide or childcare services, housekeeper, necessary due to age, infirmity, or illness. In addition, an amount equal to the other person benefit allotment must be deducted if the HH furnishes the majority of the attendant's meals. The allotment for this meal related deduction must be that in effect at the time of the most recent certification. |

|

Cost of health insurance premiums. |

|

Co-payments for appointments or prescriptions. |

|

Postage for mail-order prescriptions. |

|

Adaptive equipment in vehicles and homes as well as monthly telephone fees for amplifiers and warning signals for elderly or disabled individuals, and the costs of telecommunication devices for the elderly or disabled may be considered allowable medical expenses. |

|

Over the counter drugs, ointments or other treatments that are recommended by a licensed health care practitioner (excluding nutritional drinks or other dietary supplements). |

HHs cannot utilize the medical deduction for costs of prescribed medical marijuana or any other substances that are considered illegal under federal law.

Ineligible Medical Expenses

Certain expenses do not qualify as medical expenses under CalFresh policy. The table below provides a list of expenses that are not allowable medical expenses:

|

Ineligible Medical Expenses |

|

Special Diet food such as nutritional drinks or other dietary supplements (e.g., Boost, Ensure). |

|

Medical bills paid prior to the month of initial application. |

|

Premiums for health and accident policies (such as those payable in lump-sum settlements for death or dismemberment or income maintenance policies, such as those that continue mortgage or loan payments) while the beneficiary is disabled, are not deductible. |

|

Any Item that can be purchased with CalFresh benefits, including prescribed foods. |

|

For SSI/SSP recipients, the Medicare premium is not allowed as a medical expense as the State pays for Medicare Part A and/or B premiums. Eligibility staff are not to update Medicare Part A, Part B, or Part D premiums on the Expense List Detail page. |

Shared Living Expense Deductions/Treatment of Expenses shared with others

Shared living expenses include allowable shelter, utility and/or dependent care expenses, which the CalFresh eligible HH member’s shares with:

· An excluded/ineligible HH member; or

· Another HH which may not be participating in the CalFresh Program.

Shared Expenses and Excluded HH Members

When a CalFresh HH includes eligible/aided members and excluded members, there must be a distinction made to identify which members contribute to the expenses of the home. Contributors are those HH members who share the residence and the expense of that residence by paying or obligating money from their separate income or resources. The treatment of the expenses made by excluded HH members is strictly based on the reason for exclusion as follows:

Shared Expenses and Separate HHs

The CalFresh HH may live with a separate HH which may or may not participate in the CalFresh Program. If shelter and/or utility expenses are shared by these HHs, the expenses will be allowed for each HH. If the CalFresh eligible HH is eligible for a utility allowance, it will receive the full allowance and there will be no proration among the HHs. The utility expenses will be allowed to each of the CalFresh eligible HH(s) if they both contribute. The actual amount paid by each HH will be allowed for the actual shelter cost.

Expenses from Intentional Program Violators (IPV), Ineligible Fleeing Felons or Probation/Parole Violators, or Workfare/Work Sanctioned Individuals:

If the CalFresh HH shares deductible expenses with the above-mentioned excluded members, the entire allowable standard, medical, dependent care, and excess shelter deductions will apply to the remaining CalFresh HH members. The allowable deduction is not prorated.

Expenses from Ineligible Non-Citizens and/or Social Security Number (SSN) Disqualified Individuals:

When the above-mentioned excluded members pay part or all the deductible expenses, the expenses (except for the utility allowances) will be prorated among all CalFresh HH members, and only the eligible member’s share will be counted as the deduction.

To be considered a contributor, the ineligible non-citizen or SSN disqualified individual must be using his/her income or resources to make this contribution. Any of these members who have income must be included in the proration of the expenses:

|

If… |

Then… |

|

The HHs allowable shelter, dependent care, and expenses are paid entirely by the excluded member(s) |

The deductions will be prorated and only the CalFresh eligible member’s share will be counted as a deduction. |

|

The HHs allowable shelter, dependent care, and expenses are shared by the excluded HHs member(s) |

The excluded member’s contribution will be deducted from the expense and the net amount is the CalFresh HHs allowable deduction. |

|

The HHs allowable shelter, dependent care, and expenses cannot be differentiated (i.e., pooled income) |

The CalFresh HHs deduction amount will be counted as normal and pro-rated evenly amount the members contributing to the expense. |

Expenses from Supplemental Security Income (SSI) Recipients and/or Ineligible Students

Ineligible Students

If the CalFresh HH shares eligible expenses with members who are excluded as ineligible students, the amounts contributed by those HH members must be deducted from the allowable expense. Only the remaining dollar amount will be allowed as the CalFresh HHs deduction.

SSI Recipients

Effective June 1, 2019, SSI recipients are no longer considered excluded HH members and their contributions to expenses are treated as those of any other eligible included HH member. However, staff is to note that SSI recipients on existing CalFresh cases (prior to June 1, 2019) will continue to be excluded until the SSI recipient is added to the CalFresh HH at the HH’s next SAR 7, RC, HH’s composition change request or the HH’s voluntary request to add the SSI recipient.

Staff must follow the guidelines below to determine the contributions from the excluded HH members:

|

If… |

Then… |

|

The payments or contributions made by these excluded HH members cannot be differentiated |

The expenses will be prorated evenly among the members contributing to the expense and only the eligible CalFresh HH member’s share is counted as a deduction. |

|

Contributions from the SSI recipients or ineligible students are not made |

These individuals are not counted in the proration. |

INCOME FROM EXCLUDED HH MEMBERS

Excluded HH members are excluded in determining the CalFresh HH size, eligibility, and benefit level, but their income is counted for purposes of CalFresh eligibility determination. In certain situations, the income is partially counted, while other situations mandate for counting the entire portion of the excluded HH member’s income.

Policy mandates the income from the following CalFresh excluded populations will be counted in its entirety:

1. Disqualified due to IPV;

2. Non-compliance with work requirements/sanctioned individuals for failure to comply with CalFresh Work Requirements;

3. Ineligible Fleeing Felon; or

4. Ineligible Probation/Parole Violator.

A pro-rata share (or only a portion) of the income from the following CalFresh excluded populations will be counted as income to the remaining CalFresh HH members:

1. Ineligible Non-Citizen;

2. SSN disqualified; and

3. Able-Bodied Adults Without Dependents non-compliance sanctioned.

How this income pro-ration applies to the expenses from these excluded HH members:

· The earned income deduction will apply to the pro-rated income earned by such excluded members and then attributed to the HH.

Income from Ineligible students will not be considered available to the CalFresh HH:

INCOME AND EXPENSES FROM NON-HH MEMBERS

The income and resources of non-HH members will not be considered available to the CalFresh HH. Any cash payments from the non-HH members to the HH will be considered unearned income.

When the earned income of one or more HH members and the earned income of a non-HH member are combined, the income of the HH member will be determined as follows:

|

If… |

Then… |

|

The HHs share can be identified |

Income share will be counted as earned income to the HH. |

|

The HHs share cannot be identified |

Income will be pro-rated among all those earning the income and count the HHs pro-rated share as earned income to the HH. |

Any expenses shared with a non-HH member will be treated as follows:

· If the eligible HH member(s) lives with and shares allowable shelter, utilities and/or dependent care expenses with a non-HH member, the contribution from the non-HH member will be deducted from the appropriate expense(s) and the net amount is the HHs allowable deduction.

· When the contribution cannot be differentiated (pooled income), the eligible HHs deduction amount will be determined under the normal standards.

INCOME FROM HHs WITH BOARDERS

Individuals paying a reasonable amount for room and board are to be excluded from the HH when determining the HHs eligibility and benefit level. The treatment of income from boarders depends on the actual circumstances and are best described by the table below:

|

If… |

Then… |

||||||

|

Individual is a boarder |

The HH has the option of including this individual in their case.

|

Payments received from the boarder, except a foster care boarder, will be treated as self-employment. Please refer to the separate release for self-employment for a more detailed description of this income’s treatment under CalFresh Program.

Documentary evidence is used as the primary source of verification. Documentary evidence consists of a written confirmation of the HH’s income and/or expenses. Acceptable verification is not limited to any single type of document and may be obtained through the HH or other sources, such as a collateral contact. The HH has primary responsibility for providing verification to support statements on the application and to resolve any questionable information. HHs may supply verification in person, through the mail, through an electronic portal, or through an Authorized Representative.

Eligibility staff may refer to AR 5475, dated May 2, 2016.