|

Release Date: 05/30/19 |

|||

CALFRESH

63-502.14 Unearned Income

( ) To release a new policy

( ) To release a new form

( ) To convert existing policy to new writing style only – No concept changes

( X ) Revision of existing policy and/or form(s).

Changes are highlighted in grey throughout the document.

This policy release focuses on defining, describing, and presenting Unearned Income as it relates to CalFresh eligibility. It will discuss the following areas in detail:

2. When is Rental Income Treated as Unearned Income

3. Reasonably Anticipated Income

4. Unearned Income Recoupments

What changed?

Note: Effective June 1, 2019, Supplemental Security Income/State Supplementary Payment (SSI/SSP) recipients will no longer be considered excluded household (HH) members and their income will be counted in its entirety for CalFresh purposes. SSI/SSP income is considered unearned for CalFresh purposes.

Unearned Income is counted for purposes of determining CalFresh eligibility. Any personal income that is derived from sources other than employment is considered unearned. However, depending on the source of the income, there are some instances in which Unearned Income will not be counted. Also, unlike Earned Income, there is no income disregard applied to countable Unearned Income.

N/A

|

Term |

Description |

|

Means-tested |

This is when the HH’s financial circumstances are considered in determining eligibility and/or benefit level. These means-tested programs make publicly-funded payments to the HH: California Work Opportunity and Responsibility to Kids (CalWORKs), General Relief (GR), or SSI.

|

|

· CalWORKs payments received from assistance programs, such as, General Relief (GR), Cash Assistance Program for Immigrants (CAPI), Refugee Cash Assistance (RCA), Kinship Guardianship Assistance Payment (Kin-GAP) Program, Tribal Temporary Aid for Needy Families (TANF), or other assistance program based on need. · Annuities, pensions, retirement (regardless of the source), veteran’s benefit, adoption payments, or disability benefits. · Social Security Administration benefits, such as Retirement, Survivors, and Disability Insurance (RSDI) benefits (this also includes SSI).

Note: Effective June 1, 2019, both SSI/SSP will be considered counted Unearned Income for CalFresh purposes.

· Private disability. · Permanent and Temporary Worker’s Compensation benefits. · Unemployment Insurance Benefits (UIB). · Temporary Disability Insurance Benefits (DIB). · Deemed income from a sponsor (who has signed an I-864) paid to a sponsored non-citizen. · Income derived from owned rental property that a HH member is actively managing for an average of less than 20 hours per week. · Child or spousal/alimony support made directly to the HH from a non-HH member; this excludes support that is transferred to another agency, such as the District Attorney’s (DA) office. · Scholarships, educational grants, fellowships, deferred payment loans for education, veteran’s educational benefits and the like, which are not excluded by federal statute, as specified in Section 63-502.2(1)(4) or through application of allowable exclusions as specified in Section 63-502.2(e). · Payments from government-sponsored programs, dividends, interest, royalties, and all other direct money payment from any source which can be understood to be gain or benefit. · Monies which are withdrawn or dividends which are or could be received by a HH from an excluded trust fund (see Section 63-501.3(h). Such trust withdrawals must be considered income in the month received, unless excluded under Section 63-502.2. Dividends which the HH has the option of either receiving as income or reinvesting in the trust are to be considered as income in the month they become available to the HH, unless excluded under Section 63-502.2. · Reimbursements which exceed total expenses, or which are intended to cover living expenses, such as food, rent, and clothing. · Monies that are legally obligated and otherwise directly payable to the HH, but which are diverted by the provider of the payment to a third party for HH expense, must be counted as income and not excluded as a vendor payment. The difference is whether the person or organization making the payment on behalf of a HH is using funds that otherwise would have to be paid to the HH.

Note: This does not apply to payments made to landlords or mortgagees by the Department of Housing and Urban Development (HUD). HUD payments are excluded from income as a vendor payment. Such payments include housing and/or utility payments.

· Adoption Assistance Program (AAP) Income. · Cash gifts. · Loans without a repayment agreement. · Paid Family Leave. · Lottery winnings. · Striker benefits. · Foster Care – only when the HH chooses to include the foster care child(ren) on their CalFresh case. |

|

Other Requirements |

Limit/Condition |

|

Rental income applies when a HH owns the rental property and rents out a dwelling separate from their main residence. A room inside or in the back of the same house, would not be considered rental property.

Rental income is only considered unearned when the property owner is involved less than 20 hours per week managing the property. In this event, this will be first treated as self-employment and the gross net income is counted as Unearned Income.

If the owner is involved managing the property for more than 20 hours per week, then the income will be counted as earned income. In this event, the income will first be treated as self-employment and the gross net income counted as earned income. Please note that self-employment is discussed more thoroughly in a separate release. |

|

|

There are instances in which income (earned or unearned) may be anticipated to better determine correct eligibility. Two main factors must be present before income can be anticipated, which includes the HH being reasonably certain of:

· The amount to be received; and · The date in which the income will be received.

Note: Income cannot be reasonably anticipated, nor used for CalFresh eligibility determination if one of these two factors are missing. |

|

|

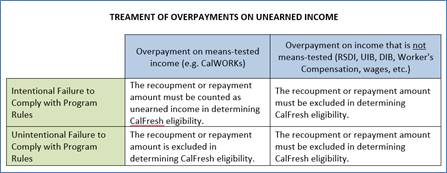

There are instances in which a portion or the entire amount of the unearned income is being withheld from the HH. Unearned Income that is withheld from a public assistance grant or income that is repaid by the recipient to the Public Assistance Program, are both considered countable Unearned Income, if the following conditions apply:

1. The income is voluntarily withheld or returned to repay a prior overpayment that was caused by the HH’s intentional failure to comply with the requirements of another federal or State means-tested program; and

2. The overpayment is not considered excluded income. When the above conditions do not apply, then the recoupment will be excluded as income.

The following table better describes this concept:

|

|

|

Unearned income from minor children |

Unearned Income from minor children is counted for CalFresh purposes. The income exclusion of children who are in school and under 18 only applies to earned income. |

|

Category |

Acceptable Documents (not an exhaustive list) |

|

Unearned Income |

1. Award letters 2. Print-outs from income source 3. Checks Stubs 4. Copies of checks 5. MEDS (for UIB/DIB/RSDI, etc.) 6. Bank Statements |